Insurance has always involved recurring payments, data-driven decision-making, and long-term relationships with individual customers. But with consumer expectations elevated by experiences with services like Netflix and Spotify, it may be time to evolve how insurers present their offering and engage with customers.

Meeting ever-increasing customer expectations

Customers now expect to access the coverage they need at the tap of a screen. In addition, insurers can now cater for previously unmet needs:

- Seamless personalisation.

- The ability to toggle extras on and off.

- Precision-based pricing based on actual behaviour.

- Automatic coverage for new purchases.

Customers expect less friction, fewer repetitive forms to fill, and faster decisions.

The way insurers collect and process information has changed, and the volume of data available has dramatically increased. For example, live driving data and GPS tracking allow car insurers to tailor premiums based on driver behaviour and mileage. Application Programming Interfaces (APIs) have made it easier to share data between services. And the commodification of machine learning makes it easier to analyse complex data and use it to make better, faster predictions.

But there are still many pitfalls and issues to work through. For example, there's a tension between the ability to harness large amounts of historical data, favouring legacy insurers, and the demand for a much slicker and faster signup, payment, and claims processes, tilting the balance towards new entrants.

How Monzo partnered with traditional players

At first glance, insurance seems to be an industry ripe for disruption, with poor digital user experiences and inefficient claims processes. But with higher barriers to entry, established insurers may want to partner with startups in adjacent industries rather than wait for competition from venture-backed startups.

One such partner is Monzo. This UK neobank has long impressed consumers and investors with its easy-to-use, app-based service. In its early stages, Monzo deliberately borrowed much in company culture and user experience from Spotify, talking to customers in small interdisciplinary teams and building desired features unavailable in the market.

Features like 24/7 chat-based customer care, with cases dealt with asynchronously at any time, rather than requiring customers to commit to calling a contact centre during work hours.

Moving to membership

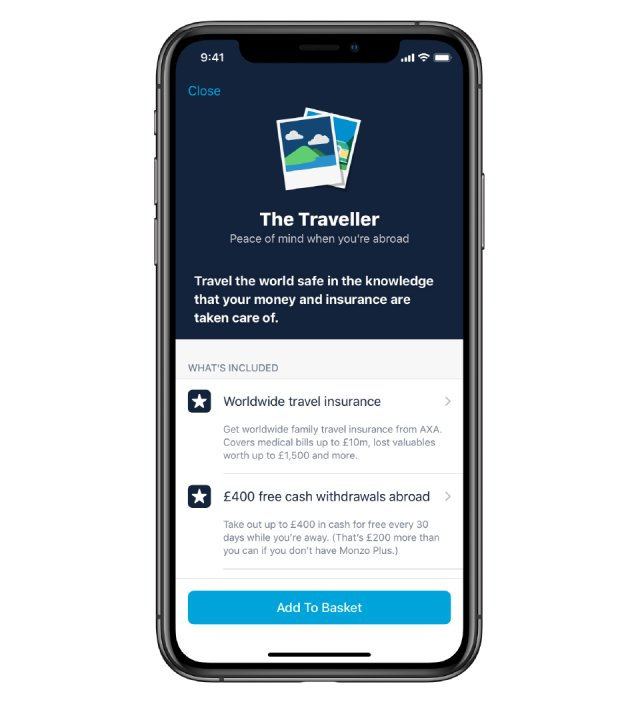

When developing a paid proposition, Monzo borrowed the language and pricing strategy of Spotify Premium, a monthly subscription model with which many of their customers were already familiar. Monzo Premium launched in 2020, bundling premium banking features and insurance in a single monthly payment. Members get worldwide mobile phone and travel insurance, including USA and Winter Sports, without paying a lump sum upfront.

With vast volumes of transactional data, players like Monzo can gently nudge customers towards adjusting their policy as needs change. For example, they can upsell additional insurance products based on recent purchases, such as buying a bicycle, leasing a car, or booking a holiday. The signup journey is simple, expertly explaining policy terms using the startup's no-nonsense brand voice. But look at the small print, and these are third party policies from AXA and Assurant, broken into a monthly fee.

Does it pay to partner?

The partnership between both parties is a smart move - AXA and Assurant get access to a younger, more digitally savvy consumer, and Monzo can move quickly, not having to learn a whole new vertical from scratch.

The problem comes with the claims process. Monzo must direct customers to phone their partner's contact centre, with all the attendant friction - busy lines at peak times, the need to reconfirm identity, and being present and synchronous on the call. This jars with the slick, app-based experience customers enjoy if they want to report a fraudulent bank transaction, change their pin, or take out a loan.

While partnering with startups enables a best-in-class front-end experience, insurers need to consider redesigning the claims process to match the experience that subscription app users expect.

How FT Strategies can help

- Building B2B relationships - we're experienced at interfacing between startups and established businesses, enabling partnerships that create new revenue streams and combine the best of both worlds.

- Digital Transformation - putting the customer front and centre to ensure that journeys between partners feel as seamless and friction-free as possible.

Monzo’s insurance and banking bundle

How Lemonade builds loyalty to drive down its loss ratio

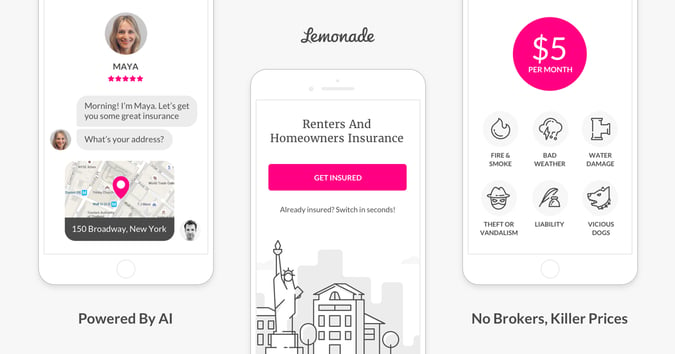

Disrupters have found the market harder to crack when going it alone. A prime example is the US Insurtech startup, Lemonade. The company initially generated excitement and viral customer acquisition with its chatbot-based signup and almost-instant claims process. However, after two years of rapid growth, the company was at a data disadvantage.

While their innovative, machine learning-based approach to claims meant quick decisions, high customer ratings, and lower operational costs, a problematic loss ratio of 160% meant a long way to go to profitability, denting investor confidence.

Innovative design and machine learning capability aren't enough. New entrants need what legacy insurers have in abundance: large amounts of historical customer data. More data means better fraud detection models and improved customer risk predictions.The challenge was acquiring a huge volume of customers and retaining them long enough to have the necessary data to build market-leading machine learning models.

Drawing on insights from behavioural economics, Lemonade opted for monthly payment and a flat fee structure, with any money left over after claims and fees donated to a good cause of the customer's choice. This structure creates a less adversarial relationship between insurer and insuree, leading to increased brand loyalty and reduced propensity to claim fraudulently.

Lemonade's loss ratio hasn't yet fallen below 60%, a typical break-even point, because of the decision to enter new markets like car insurance. But with a best-in-class net promoter score, improving levels of customer retention, and robust performance in cross-selling additional insurance products, the scale-up is betting it can gain a data advantage quicker than incumbents can develop the same capabilities.

How FT Strategies can help

- Acquire Customers - identify the pain points of new customers and develop winning pricing strategies and propositions.

- Improve Retention - understand the triggers for customer churn, so you can create loyalty and retain customers for the long term.

Lemonade’s disruptive offer for renters and homeowners

Lemonade’s disruptive offer for renters and homeownersHow Laka builds community to increase honesty and loyalty

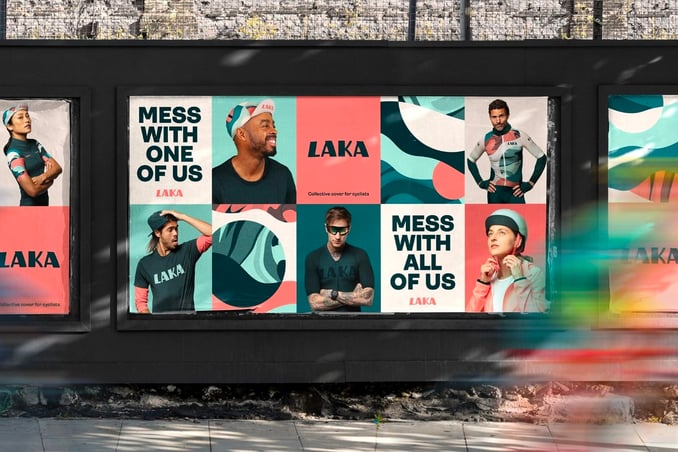

Digital-first cycle insurer Laka sees insurance as a team sport: a communal safety net for professional and amateur cyclists alike. Members are encouraged to take greater responsibility for protecting their bicycles and cycling equipment. And they are encouraged to think about the broader group before making claims.

A variable pricing strategy is at the centre of this: if claims are lower in a given month, Laka passes this saving on to members. But, conversely, the monthly price will be a little more if claims are higher. The insurer is testing the idea that a community-led model will result in fewer fraudulent claims by consistently reminding members that they are part of a collective, both through the increase and decrease of monthly payments and through consistent brand storytelling.

With compelling social media and email marketing and automation, Laka upsells specialist health and third-party liability insurance and has moved into last-mile delivery insurance.

How FT Strategies can help

- Drive Engagement - develop a membership strategy to create highly engaged customers, reducing churn and increasing lifetime value.

- Create valuable recurring revenue - create a compelling pricing strategy taking in dynamic pricing, lifetime value modelling, and cross-selling and upselling.

Laka’s bold message of collective group identity is revolutionising bike insurance

Laka’s bold message of collective group identity is revolutionising bike insurance